On the 8th of February, OCI LAB incubator hosted the sixth online lab: “Financial model validation” with the assistance of OCI Lab Mentor Mr. @Heni.Htira, operations coordinator on CVE programs, alumnus advisor and a judge in the Enactus national competition.

During this lab, Mr. Heni gave a detailed presentation illustrated by various examples to help a project leader build and validate their financial model.

Around 4 p.m, the participants were asked by the moderator @khouloud.ouesleti to do the check-in as usual via the zoom conference room by writing their full names, countries, and projects in the chat channel.

At first, Mr.Heni displayed the agenda for this lab and then started highlighting the importance of building a financial model for your business. He defines it as a critical tool used by organizations to understand business risks and make critical strategic decisions. In fact, there are specific keywords linked to financial modeling: Decision making, Assumptions, Model, design, Developing, etc. Yet they all occur in one Excel sheet.

Indeed, a robust and flexible model can be described as the art of combining accounting finance and business metrics to build a representation of your company to excel in the future.

The reason why a business needs a financial model is to study a company’s financial history and to use the history and the information available to predict the company’s performance in the future. Therefore, you can learn a lot about a company’s revenue growth profile, cost structure, margins, and earnings growth by analyzing its past performance.

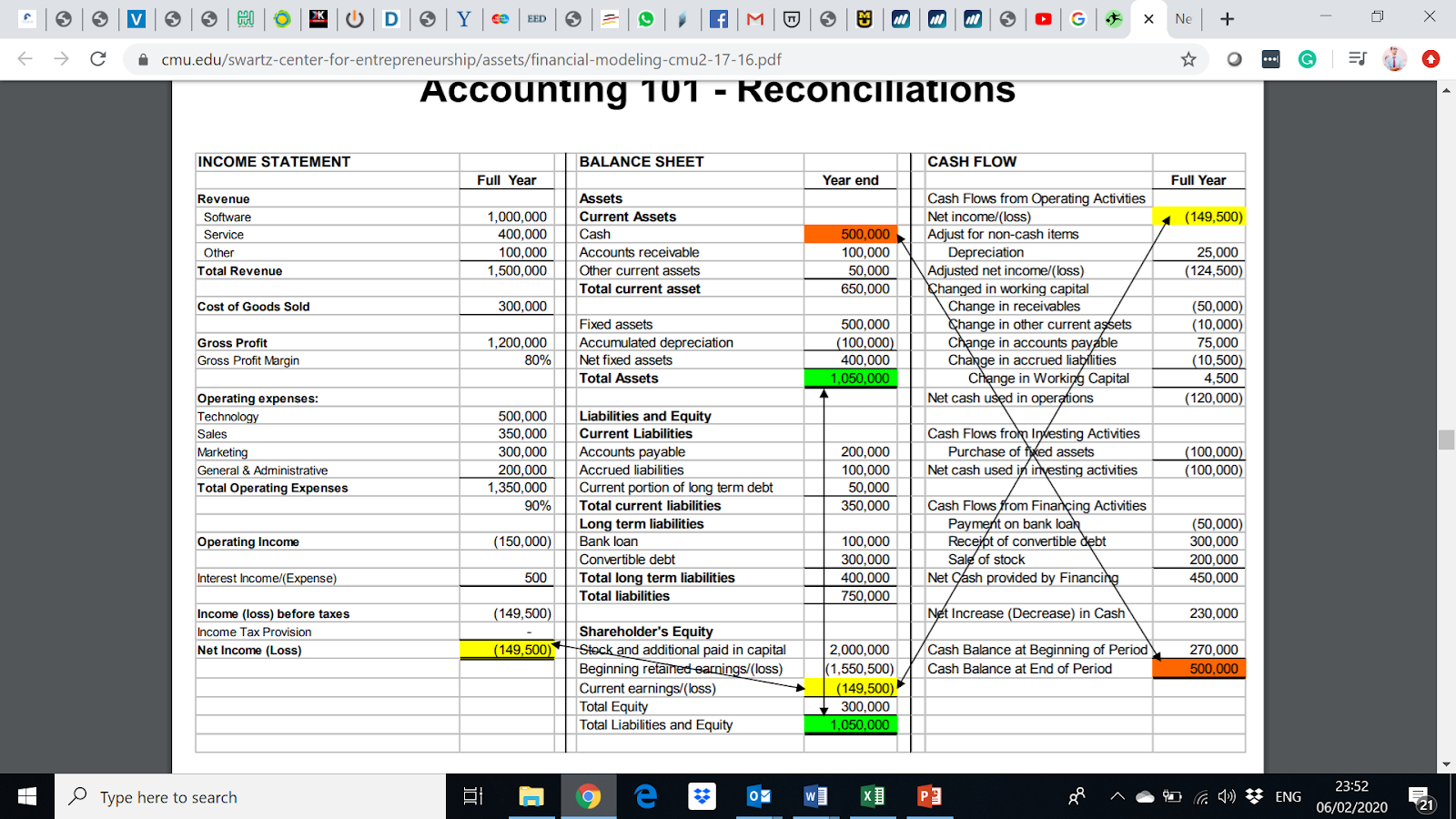

The most basic financial model is a 3-way model that refers to the three financial statements named an Income Statement, Cash Flow, and, most importantly, a Balance Sheet.

As a matter of fact, the most common use of these models is for the decision making usually in an operating Company, Corporate division, finance, and accounting staff, Etc. Also, it is used to make investment decisions in a given company. Additional use is for price security. It is mainly for companies desiring to issue more shares or further debts.

Thus, they need a financial model to value these securities. Besides, it might be the ability to project working capital requirements into the future accurately.

As for who uses financial modeling, it would-be analysts in investment banking, equity researchers, credit analyst, managers, and finance people…

Considering the steps that ought to be followed in building a financial model, one should start by taking historical data and storing it in an Excel file; it should be at least three years of information.

The second step is to calculate historical ratios, metrics, turnover rates… It can serve as foresight on what the future holds for your business.

Once you have analyzed the past, you can decide in terms of margin, growth rate, capital spending.

The following step is forecasting, the most important one, which is mainly decision making, which allows you to reflect all these numbers into the future to make efficient predictions. Typically, the forecast is 3 to 5 years long.

The final step is the Valuation. It means valuing the company or the business to come up with robust ideas or decisions. To do that, most companies use Discounted Cash flow (DCF). Then, an additional analysis might be added to support the types used, such as charts and graphs.

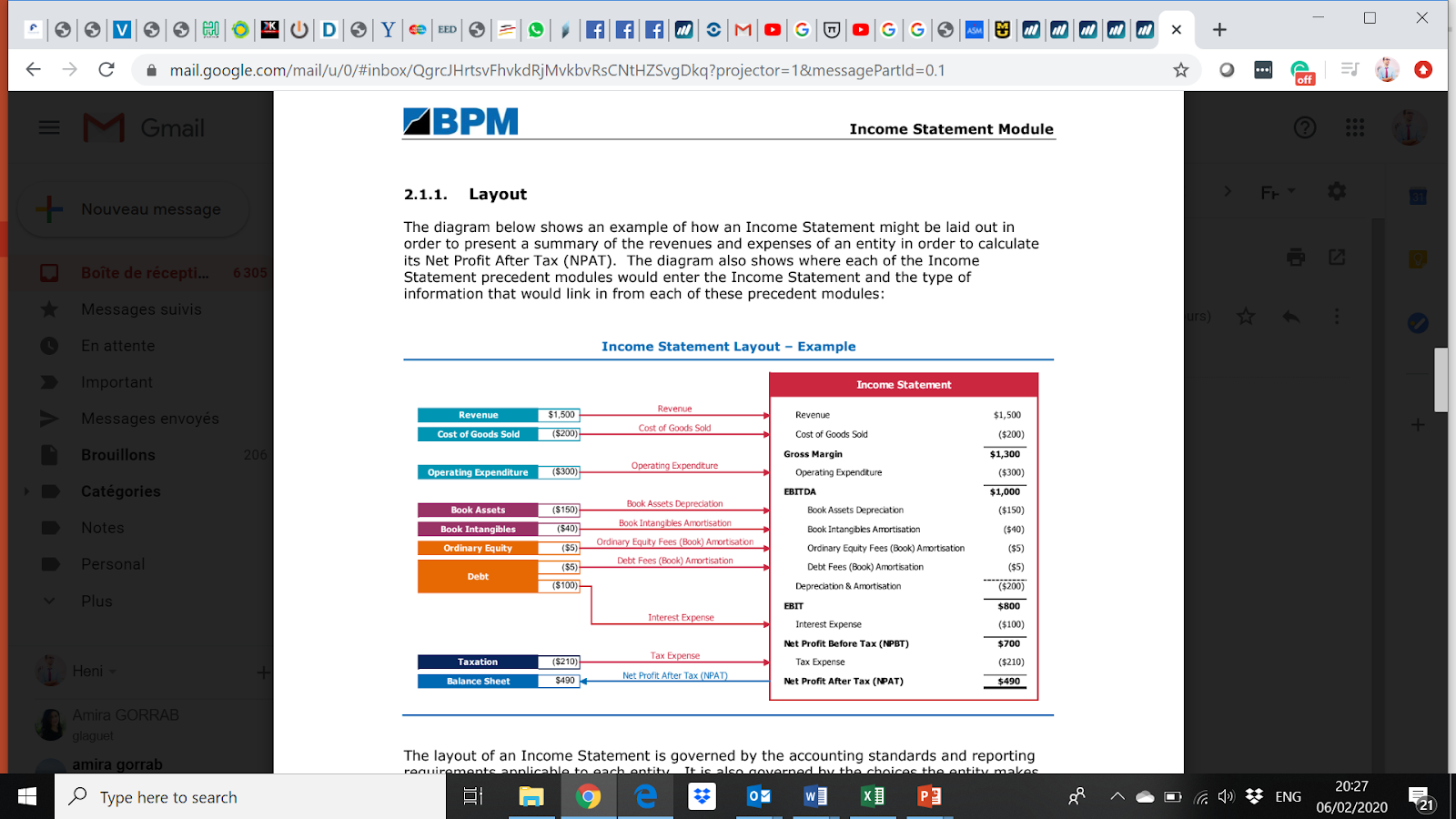

As for the three statement-model, the first element is the income statement, also referred to as a “Statement of Financial Performance‟ or a “Profit & Loss Statement,‟ which provides a summary of the revenues, costs, and expenses of an entity during an accounting period. It is generally used to calculate the Net Profit After Tax (NPAT) of an entity.

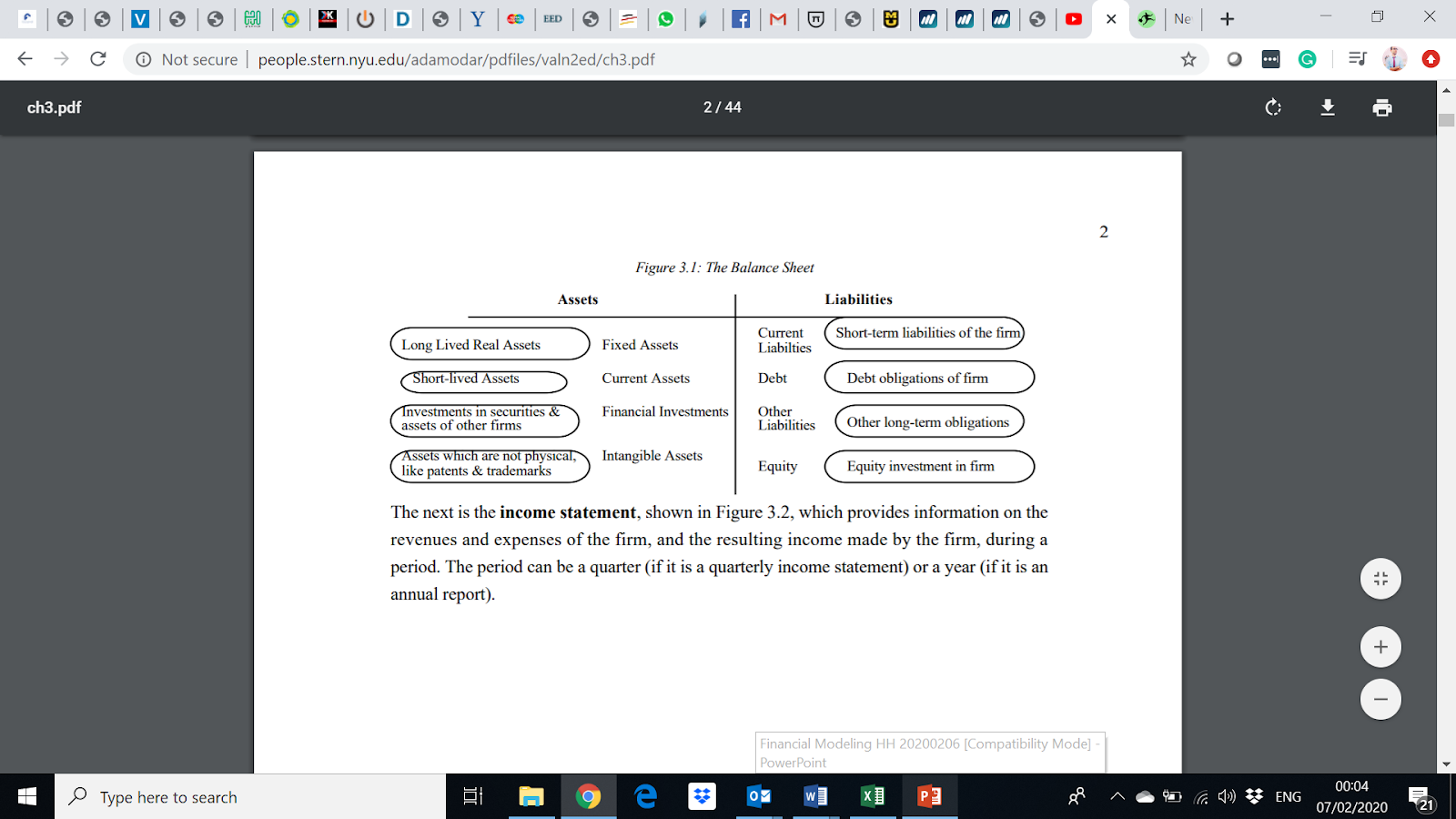

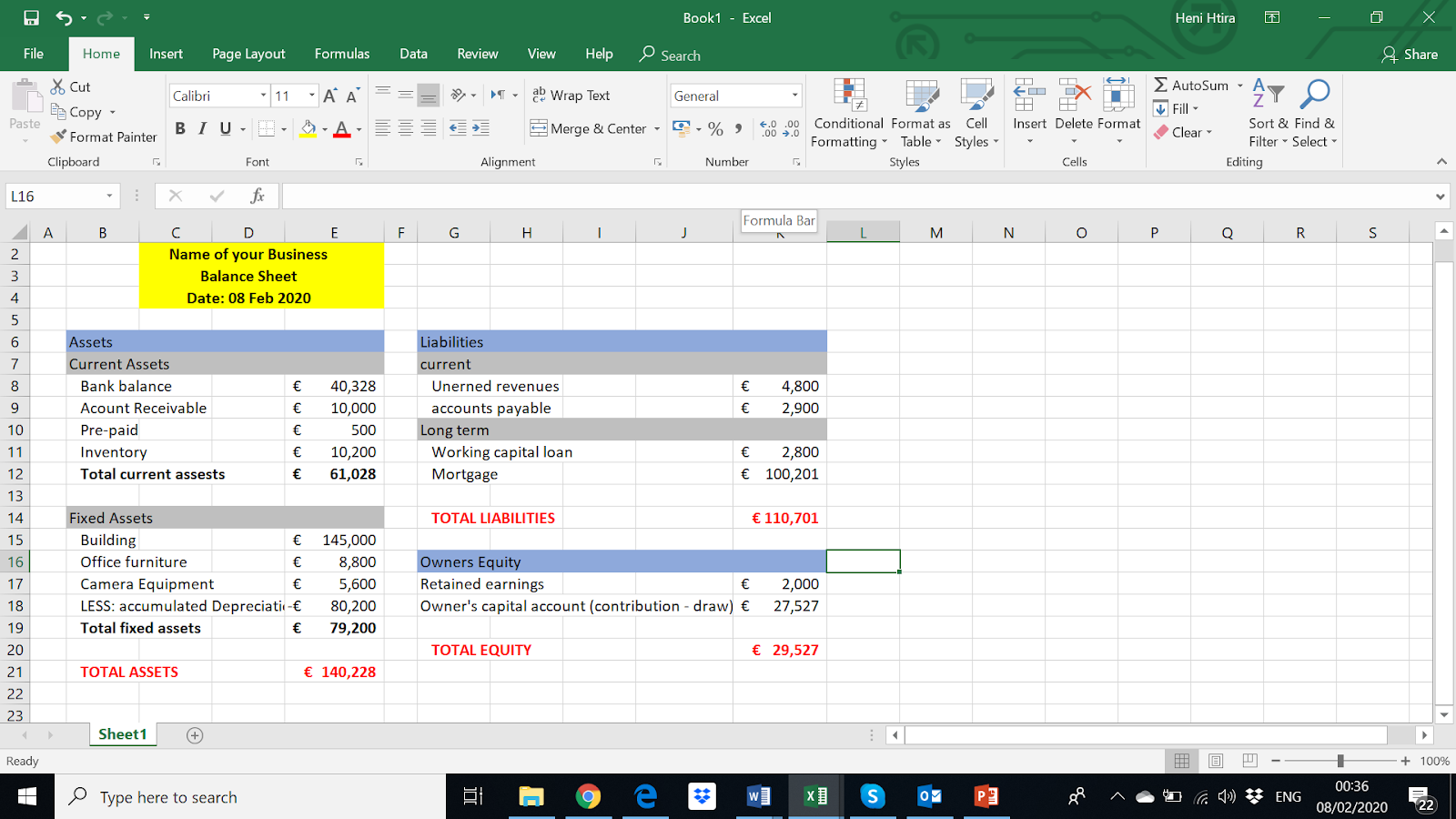

Next, there is the Balance Sheet, also referred to as a Statement of Financial Position

that shows the status of an entity’s assets, liabilities, and Owner’s equity at a point in time, usually the close of a month.

It provides a snapshot of the entity’s financial position, including the cumulative results of the Income Statement and Cash Flow Statement at a point in time. It is essential for getting investors, securing a loan, or selling even your business.

While income statement reports profitability, balance sheets represent the value of the business.

Furthermore, the balance sheet has three sections: assets that are equal to Liabilities and Owner’s equity.

Mr. Heni brought to the attendees’ attention that unlike the other statements that reflect costs and revenues in a given period, the balance sheet is an instant report, a snapshot in time at any given point, where the business stands.

The following figure shows the elements of a balance sheet:

The final statement is the statement of Cash Flows (SCF), which breaks the analysis down according to operating, investing, and financing activities. It also shows how changes in Income Statement and Balance Sheet accounts affect cash and cash equivalents during an accounting period.

Then he displayed a metaphor to illustrate the cash flow according to the figure down below, stating if the water balance (or cash balance) rises, then there is a cash INFLOW, if the balance decreases in the current period, then it’s an OUTFLOW.

Moreover, it is essential to mention that Cash Flow Statement contains: operational activities, investment activities, and financial activities

.

Operational activities are the activities that constitute the primary or main activities of an enterprise. As for Investing activities, they represent the acquisition and disposal of long-term assets and other investments not included in cash equivalents. Last but not least, financing activities relate to long-term funds or capital of an enterprise, e.g., cash proceeds from the issue of equity shares, debentures, raising long-term bank loans, repayment of bank loans, etc.

Towards the end of the lab, Mr.Heni concluded by explaining the most important valuation methodologies of measuring the cash flow of a project. Unlike traditional techniques, discounted cash flow (DCF) valuations take into account the specific financial performance of all future years.

However, such valuations are very sensitive to small changes in input data and while providing the scrupulous analyst with a potent tool. DCF takes the cash flows from the 3 statement model, alter the necessary parts, and then uses the XNPV function in Excel to discount them back to today at the company’s Weighted Average Cost of Capital (WACC).

Certainly, the advantage of a DCF valuation is that it allows the free cash flows that occur in all future years to be valued, giving the ‘true’ or ‘intrinsic’ value of the business.

He finally gave some tips to build an efficient and simple model. For instance, the model should be simple, well structured using a good layout while indicating the drivers, assumptions, and visual outputs.

Although, one needs to acquire some skills to make an excellent remarkable financial model such as Finance and accounting, Excel skills, Logic, and design.

Special thanks to Mr. Heni Htira and for the relevant interaction from our brilliant project leaders for ensuring such a productive and successful lab.

The offline task is: '‘Based on this training, Design and Develop your 3-statement-financial-model for your project.’'

Q/A section:

Q(@saif.eddine.laalej : Is there an online tool for valuation or maybe a file?

A: I don’t think there is an online tool because the tool you are using comes from your work; it should be adapted to your own business data.

Q:(@Mohsen ) Can you explain again what COGS means?

A: Cost of goods sold (COGS), it refers to the direct costs of producing the goods sold by a company. This amount includes the cost of the materials and labor directly used to create the good. It excludes indirect expenses, such as distribution costs and sales force costs.

Q: (@ Ben Ameur Mohamed Ali)

On page 21, in the excel sheet, under fixed assets, I didn’t get the term “LESS accumulated depreciation?

A: In french, it’s called “amortissement”, it is the expenses that have been taken until today for those fixed assets. Eventually, the depreciation amount can become at a certain time equal to the total amount of the fixed assets, which means total fixed assets would be 0).

Q: (@Mohsen) Should we work on two assumptions for the next three years? In the financial model? For example, an optimistic hypothesis and another pessimistic one in consumption and profits?

A: You may work on each one separately then compare. Still, you can work on whichever assumption; it shouldn’t be a problem as long as your model is logical and efficient enough.

Q:(@salaheddine ) What is the best way to define the product price? What should we take into consideration?

A: Well, there are many factors; it depends on the product because there are different strategies. Market research will help you do this; it will help you know the psychological price of your product. According to the content of the last lab, it will help you achieve that.